How to Verify Tax Free OT for 2025

Many individuals work long hours—far beyond the standard 40-hour week. Starting with tax year 2025, a tax provision in the One Big Beautiful Bill Act (OBBBA) allows many of those hard-earned overtime dollars to be deducted from federal taxable income—but only the premium portion of the overtime pay.

In this post, Angela Holmes (my personal CPA) and I break down the following:

What the OBBBA Overtime Deduction Is (and Isn’t)

The reality for 2025

How to find the amount you can deduct

How to claim the deduction on your return

Why this is extra tricky for many employees with atypical schedules

What comes next in 2026

What the OBBBA Overtime Deduction Is (and Isn’t)

Under the new law, individuals may deduct from federal taxable income the portion of overtime compensation that exceeds their regular rate of pay — generally, the “premium” part of time-and-a-half overtime (or any amount paid over your regular rate). This provision applies for tax years 2025 through 2028.

I’ve already covered the basics of this in my initial blog post regarding the OBBBA here: Understanding the Overtime Tax Break and Senior Deduction in the One Big Beautiful Bill Act.

If you normally earn $40/hour and receive $60/hour for overtime, the extra $20/hour is potentially deductible

This is a deduction, not a credit — it lowers taxable income rather than giving a dollar-for-dollar reduction in the income tax you owe

The maximum deduction is $12.5K for single filers or $25K for joint filers each year

The deduction phases out for higher income: Modified Adjusted Income over $150K for individuals or $300K for joint filers

It’s critical to remember that the deduction applies only to overtime required under the Fair Labor Standards Act (FLSA) — certain state or contractual OT definitions could not qualify unless they align with FLSA requirements

IRS Reporting Reality: 2025 is a Transition Year

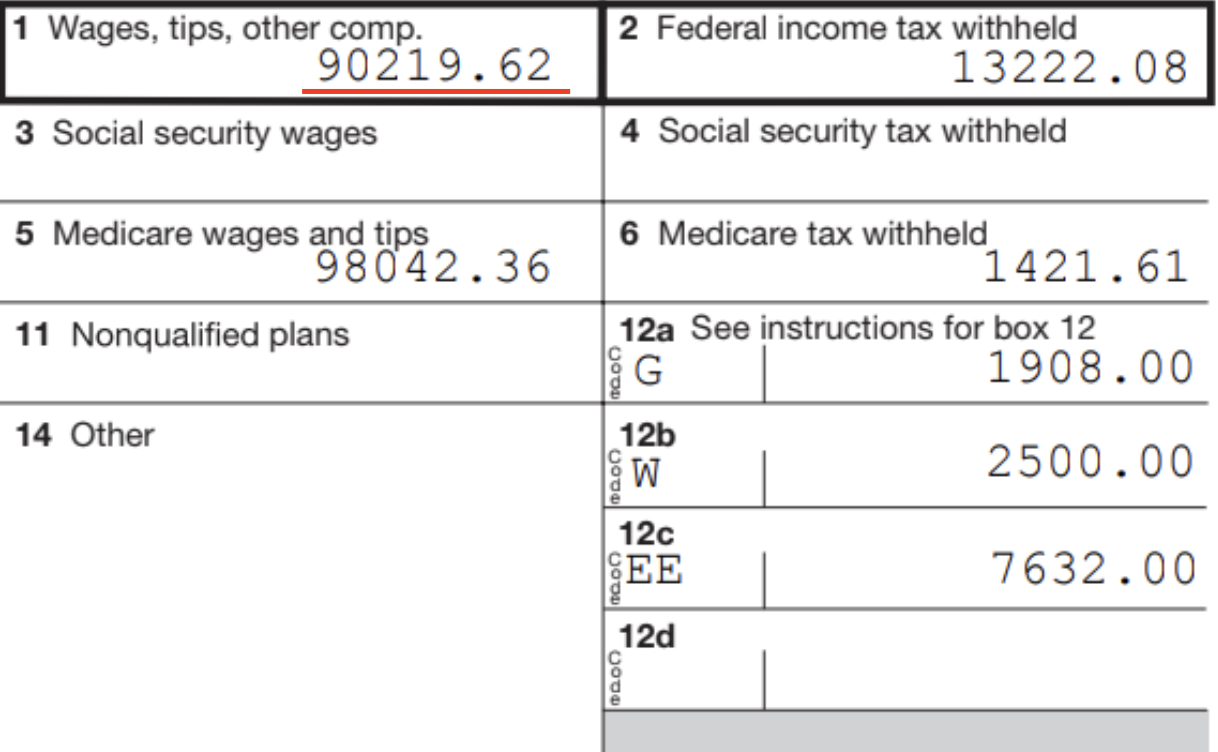

For 2025 only, the IRS will not require employers to separately report the overtime premium amount on W-2 or 1099 forms. That means the amount you see in “Box 1” of your W-2 will likely include both base pay and qualified overtime together — and you’ll have to break it out yourself to claim the deduction.

The deductible portion may be reported in Box 14 or on a separate statement, though your employer is not required to provide either.

W2 Box 1

This phased implementation gives the IRS, employers, and tax pros time to implement changes effectively.

From IRS Notice 2025-69:

“Employers and payroll providers are not required to separately account for qualified overtime compensation on W-2s for 2025. Taxpayers must calculate the qualified overtime amount using a reasonable method when reporting it on their tax return.”

How to Find the Amount you can Deduct

For many of us, it’ll be a matter of locating the 1.5x OT amount on your last paystub for 2025 and dividing by 3 to isolate the “premium” amount for tax return purposes.

Example:

Many firefighters work 24-on, 48-off with a Kelly Day (this averages out to a 48-hour work week). For all unscheduled hours worked in a 21-day work period over 144 hours and up to 159 hours, firefighters will receive overtime pay at a straight time rate.

Per FLSA, for unscheduled hours worked that exceed 159 hours in a 21-day work period, firefighters will receive overtime pay at the rate of 1.5 times their regular rate. This is the dollar amount we need for the calculation.

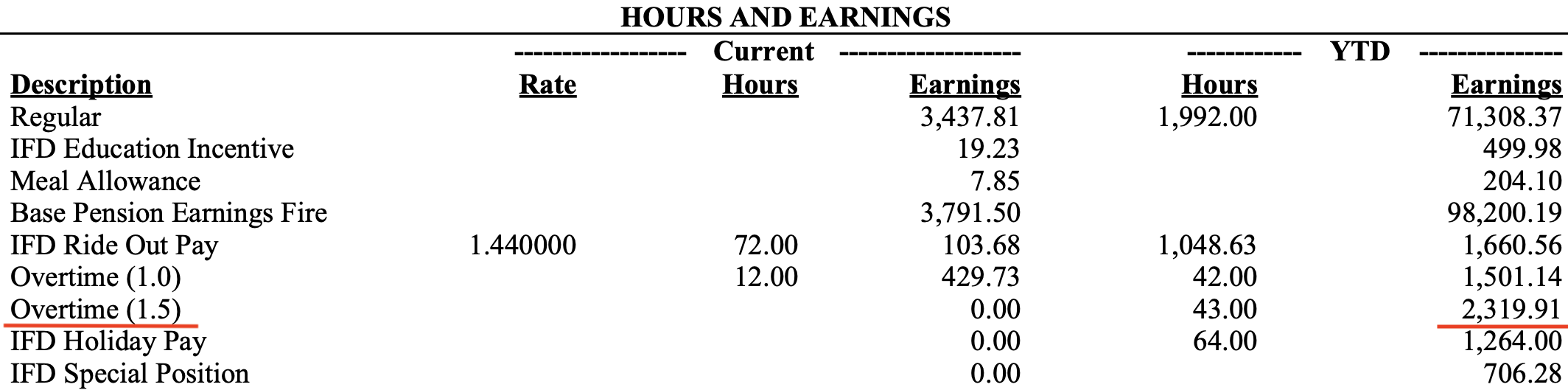

Step 1: Take a look at your last pay stub for 2025. It likely shows something similar to the “Overtime (1.5)” illustrated below.

Firefighter Pay Stub

This means $2319.91 of premium overtime was received for 2025.

Step 2: $2319.91 ÷ 3 = $773.30 tax-deductible “half” part of “time and a half” overtime

Why divide by three? Because:

2 parts represent your regular rate

1 part represents the overtime premium eligible for deduction

This same divide-by-3 approach is shown in IRS Notice 2025-69, Example 5:

“Individual C works in law enforcement and is paid $15,000 of total annual overtime pay on a ‘work period’ basis of 14 days that complies with section 207(k) of the FLSA. For purposes of determining the amount of qualified overtime compensation received in tax year 2025, Individual C may include $5,000 ($15,000 divided by 3).”

Claiming the Deduction on Your Return

In 2025, the IRS has created a new Schedule 1-A for this deduction, which will be attached to your Form 1040.

Key filing notes:

Your Social Security number must be valid and included on the return

If married, you must file a joint return to claim the deduction

Both standard deduction and itemizers may claim the overtime deduction

Because employers are not required to separately report qualified overtime in 2025, you’ll want to save pay stubs or other records showing the proper amount of deductible overtime pay in case the IRS asks.

Unique Challenge for Employees with Atypical Schedules

Federal firefighters work a lot — on average, 72 hours a week.

For most federal firefighters, “in-tour” overtime makes up the majority of their qualified overtime. Even if you worked a full year with zero extra OT, you still earned roughly 988 hours of FLSA-required in-tour overtime.

Here's the math behind in-tour overtime:

Standard tour: 144 hours in a 2 week pay period

FSLA overtime threshold: 106 hours

FLSA-required in-tour overtime:

144 hours − 106 hours = 38 hours per pay period

38 hours × 26 pay periods = 988 hours

That 988 hours isn’t optional – it’s overtime required by FSLA — and that’s exactly the type of overtime with a “premium” that qualifies for the deduction under OBBBA.

What you should do:

Pull all 26 LES statements for 2025

Add up all overtime compensation, including:

In-tour overtime

Any additional overtime

Divide that total by 3

That final number is your deductible amount.

Example:

A federal firefighter works a standard 144-hour tour every pay period for all 26 pay periods and picks up 2 additional 24 hour shifts of OT. Their regular hourly rate is $23.60.

In-tour overtime (each pay period):

38 hours × $23.60 × 1.5 = $1,345.20 OT in-tour (seen on their pay stub below)

Federal Firefighter In-Tour OT

Premium portion: $1,345.2 ÷ 3 = $448.40

$448.40 premium portion × 26 pay periods = $11,658.40 OT in-tour for 2025

2 additional OT shifts (48 hours):

48 hours × $23.60 × 1.5 = $1,699.20

Premium portion: $1,699.20 ÷ 3 = $566.40 additional OT for 2025

$11,658.40 (in-tour OT premium) + $566.40 (additional OT premium) = $12,224.80 tax deduction

If you’re married filing jointly and in the 24% tax bracket, that’s a tax savings of $2,933.95 - not bad!

If you’re a federal firefighter, Matt Stelmaszek has even more detailed content at https://www.stellarwm.com/articles breaking down the calculations, the tracking challenges, and what to do if you got promoted or changed positions during the year.

What Comes Next: 2026 Reporting Changes

Starting with tax year 2026, employers will be required to separately report qualified overtime compensation on W-2s and related forms — simplifying the calculation for taxpayers.

For the 2026 tax year, tax-free overtime will be reported on Form W-2, Box 12, using Code TT.

That makes 2025 the year you’ll likely need to do the math yourself. TurboTax or other DIY software is unlikely to help you properly calculate your OT tax deduction. If you’re not already, this may be the year working with a CPA or certified tax preparer is extra valuable!